Key takeaways

The era of ESG storytelling is ending and we’re entering a new phase. One that is increasingly becoming defined by data, documentation, and assurance. With frameworks like the CSRD, EU Taxonomy, and ISSB S1/S2 coming into force, ESG reporting is no longer just a recurrent exercise. It’s becoming a regulated, auditable function, and companies will increasingly need to demonstrate that their sustainability data holds up under third-party assurance.

So the question is: Is your ESG data audit-ready?

Sustainability reporting has rapidly evolved — from informal disclosures to regulated, third-party assured data. Here’s what that journey looks like:

From Voluntary Disclosures to Auditable ESG Reporting

The shift in ESG reporting isn’t just theoretical — it’s reshaping how organizations collect, manage, and report ESG data.

From Reporting to Assurance: The New Compliance Normal

Until now, ESG reporting was at times voluntary, fragmented, and qualitative. But as regulators and investors demand more reliability, sustainability data is now being pulled into the same governance standards as financial data.

In the EU, the Corporate Sustainability Reporting Directive (CSRD) will require companies to have their sustainability disclosures externally verified, starting with limited assurance from 2025. Over time, the bar will rise to a stricter “reasonable assurance” level, similar to what’s expected for financial audits. Globally, new standards like the ISSB’s IFRS S1 and S2 are also setting the stage for assurance to become a core part of ESG reporting.

This shift marks a turning point: it’s no longer just about what you report, but about how verifiable your data is.

What Does ESG Assurance Involve?

Unlike traditional internal reviews or ESG ratings, assurance is a formal third-party audit process. Here's what that means in practice:

- Limited Assurance

A high-level check that gives moderate confidence in the accuracy of reported data. This is the current requirement under CSRD. - Reasonable Assurance

A deeper, more rigorous review, equivalent to a financial audit, is expected to become the standard in the next few years. - Assurance Providers

Typically performed by traditional audit firms (e.g., EY, PwC, Deloitte, KPMG) or specialized sustainability assurance providers. - Audit Scope

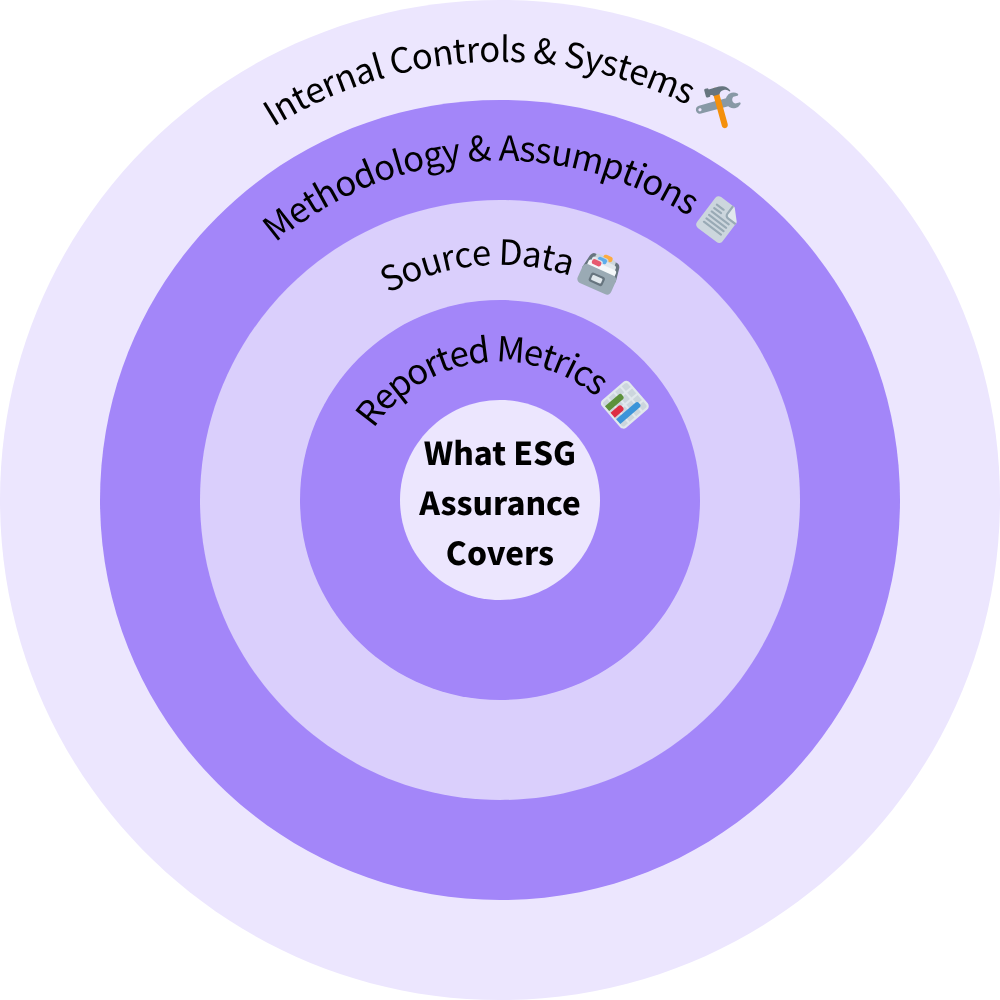

Goes beyond the headline ESG KPIs to evaluate:- Source data (i.e., meter readings, HR databases)

- Methodologies and estimates

- Data governance processes

- System-level controls

What Actually Gets Audited?

If your organization is preparing for assurance, here are the key areas that will be under the microscope that you should keep an eye on:

- Greenhouse gas (GHG) emissions (Scope 1, 2, and in many cases Scope 3)

- EU Taxonomy alignment (particularly CapEx, OpEx, and turnover alignment)

- Diversity, equity, and inclusion (DEI) metrics

- Energy, water, and waste data

- Sustainable investment claims under SFDR

But assurance isn’t just about the numbers. Auditors will assess your data trail. What’s that you may ask?

A data trail shows how each figure was calculated, where it came from, and whether there’s adequate documentation and controls to support it.

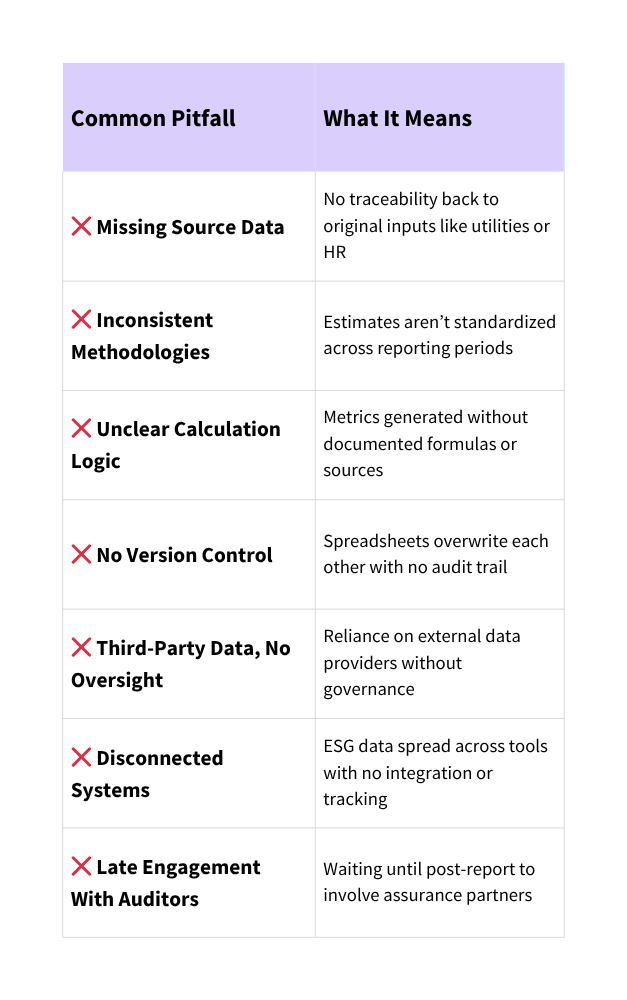

Common Pitfalls That Undermine Assurance

Many organizations are caught off guard when it’s time to validate their ESG disclosures. Here are the most common issues that slow or even fail audits:

Many sustainability teams find that while their internal reporting is solid, it still needs refinement to pass assurance requirements.

How to Get Your ESG Data Audit-Ready

To prepare for third-party assurance, organizations need to treat ESG data like financial data. Structured, controlled, and verifiable.

Here are key actions to take now:

What’s Coming Next

The pressure for assurance is only going to increase. Here’s what to keep an eye on:

- Shift from limited to reasonable assurance under CSRD (by ~2028)

- Broader coverage of ESG metrics under assurance scopes

- Growing convergence between financial and sustainability audits

- New tooling to support ESG data assurance: from platforms to AI-driven validation

- Investor pressure for verified data across portfolios

Final Thoughts: ESG Assurance Is the New Normal

There is no doubt that we’re seeing a progressive shift from a world of ESG narratives to one of ESG evidence. The organizations that will thrive in this new environment are those who recognize that transparency without traceability is no longer enough. It’s the bare minimum.

The good news? If you invest in getting your ESG data house in order now, you’ll not only meet assurance requirements, but you’ll also unlock credibility, efficiency, and trust across all your stakeholders. And much more..

Want a simpler path to ESG audit readiness?

See how Datia supports compliance teams preparing for CSRD, EU Taxonomy, and third-party assurance by clicking here.